Although the largest economy in East Africa reversed seven consecutive quarters of declining GDP to register 5.3% growth in the first quarter of the year, experts are warning policymakers against falling victim to a complacency bubble.

The middle class in Kenya is becoming poorer due to inflation-adjusted pay cuts, and businesses are defaulting on loans as interest rates reach levels last seen seven years ago.

A court decision on whether the government can implement a number of new taxing measures, such as doubling the value-added tax on fuel and withholding 1.5% of employees’ gross wages to fund affordable housing, is still pending as of one month into the new fiscal year.

President William Ruto’s administration will be put to the test as to whether or not it can keep the campaign promises it made to Kenyans given the delay in implementing the provisions in the Finance Act 2023.

The “crunchy economic times are going to get crunchier,” according to public policy researcher Robert Shaw, unless the government develops and puts into action a stronger policy to prevent the economy from deviating from its intended track.

The way things are going right now is the wrong way. Our government has a voracious appetite for both increasing revenue and increasing spending. That almost feels like a self-inflicted injury,” Mr. Shaw observes.

“The court case and the current protests raise questions. Economic activity is being affected by the protests, and the economic recovery is in jeopardy. Investors will refrain if protests continue for a long time.

Mr. Shaw cautions that even if politicians are not present, the mass movement could “get a life of its own” if people use it to express their resentment at the high cost of living and the widespread unemployment.

Kenya Revenue Authority (KRA) has been entrusted by the government to raise Ksh2.57 trillion to assist fund a Ksh3.58 trillion budget for the fiscal year that began on July 1.

With a fiscal year ending in June 2022, the KRA missed its tax collection target by Ksh107 billion and cited a challenging economic environment as the reason.

Ksh2.166 trillion was collected by the taxman, a 95.3% performance rate. Ksh2.273 trillion was the desired amount. Reduced tax revenue might force the government, which had a debt of Ksh9.63 trillion as of the end of April, to increase borrowing or cut development investment, both of which would be detrimental to growth.

This occurs when Kenya’s first Eurobond’s Ksh280 billion bullet payment draws near.

The Treasury anticipates that Kenya’s economy will grow by 5.5% in 2023, up from 4.8% the previous year, but is aware that more people are already having to deal with rising prices for necessities, including food, electricity, and transportation.

Njuguna Ndung’u, the Treasury Cabinet Secretary, has stated that “urgent and decisive interventions”—particularly on the supply side—will be needed to address the spike in food insecurity and the increase in living expenses.

However, Ken Gichinga, the head economist at Mentoria Economics, predicts that the resurgence of opposition-led street protests and warnings of a protracted period of civil disobedience would bring more gloom to the economy.

“We are currently facing multiple layers of tightening, both on the monetary and fiscal policy sides, which is why the outlook predicts a slowdown. The situation becomes even more hazy when political risk is included,” according to Mr. Gichinga.

Foreign investors have historically reduced or halted new investments due to political upheaval and terrorist activities associated with Al Shaabab in northern Kenya.

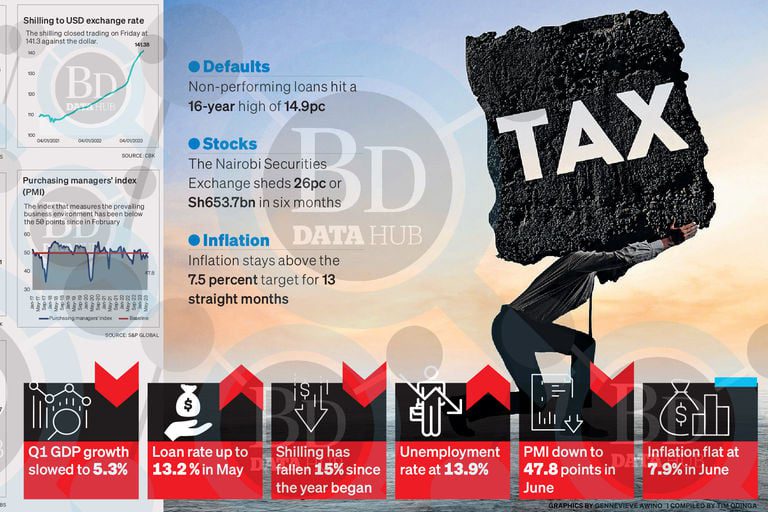

In the first half of the year, the Nairobi Securities Exchange lost 26% of investors’ wealth, or Ksh653.7 billion.

The demonstrators are expressing their displeasure with the impending implementation of additional taxes as well as the rising costs of goods like sugar and fuel.

With the government’s intended range of between 2.5% and 7.5% for inflation being exceeded for 13 consecutive months, by the June inflation rate of 7.9%, Kenya’s cost of living pressure is proving to be wider and more enduring than initially anticipated.

Kenya relies on rain-fed agriculture, therefore a lack of rain could derail Dr. Ruto’s proposal to increase productivity by paying farmers more.

According to official figures, Kenya’s food import bill in the first quarter of the year was Ksh80.2 billion, virtually matching the Ksh87.5 billion in food export revenue, putting the nation’s status as a net food exporter in jeopardy.

As a result, Kenya is still vulnerable to changes in the price of imports of foods like rice, wheat, and maize, which could put pressure on the foreign currency and result in unpaid taxes due to waivers given to importers.

Banks are also predicting slow growth and a decline in purchasing power after the Finance Act takes effect.

The new tax laws, according to Equity Group Chief Economist and Director of Research Yvonne Mhango, speak to tightening fiscal policy, which when combined with the current rise in interest rates will temper economic growth.

“Households will have less discretionary income if taxes are higher. We therefore anticipate a decrease in expenditure, which will have an impact on GDP growth. Businesses’ ability to reinvest retained earnings will slow down as a result, which will ultimately harm growth expectations,” according to Ms. Mhango at a recent investor meeting on equity.

Given the consistent increase in T-bond and T-bill yields, banks’ interest for government papers has been growing.

For instance, a new five-year paper has a coupon rate of 16.84%, which poses a risk to people and businesses looking for bank loans.

In keeping with the central bank rate, which is currently at 10.5%—the highest level in nearly seven years—commercial banks have been increasing their loan amounts.

In the private sector, where the non-performing loans ratio touched a 16-year high of 14.9% in May, Mr. Gichinga anticipates banks would focus more on the government.

Investors will eventually start to question whether the Treasury will be able to generate enough money to pay its creditors on schedule, according to him, as rates on government debt rise.

According to Mr. Gichinga, “when the moment is right, investors using risk models will begin to wonder how the government would be able to raise money to pay off debt redemptions when the enterprises that are meant to do so are having trouble.”

The government has experienced difficulties in making timely payments to civil officials and releasing funds for other crucial tasks like managing counties, paying retiree pensions, and paying hospital expenses for those covered by the National Health Insurance Fund (NHIF).